Renters Insurance: What Landlords Need to Know

Guide to Renters Insurance

What is Renters Insurance?

Renters insurance is a type of policy your tenants purchase that covers their personal property and belongings in case of unfortunate events such as natural disasters, theft and fires. This insurance will also cover the cost of temporary living arrangements if a tenant's home becomes inhabitable after an incident.

Depending on the policy and the location of the property, your tenants may be able to choose from other add-on coverages. For example, tenants in California can opt to add earthquake coverage to their rental insurance properties, as not all plans include it.

What Does Renters Insurance Cover?

Landlords and tenants should be familiar with what renters insurance will cover. While the exact coverage will depend on the specific policy, most standard plans will include the following four types of coverage.

1. Personal Property

The first thing renters insurance will cover is your tenants' property, including belongings and vehicles that get lost or damaged on the property due to perils such as:

- Fire and smoke damage

- Theft and vandalism

- Leaks and plumbing-related water damage

- Lightning, hail and windstorms

- Riots, explosions and volcanic eruptions

- Damage from a vehicle or aircraft that is not yours

- Freezing or malfunctioning household systems such as plumbing, heating, air conditioning or short-circuiting electrical appliances

- Falling objects and the weight of snow, sleet and ice

Your tenants will choose the amount of coverage they need based on how much they think their belongings are worth — the more coverage they purchase, the higher their monthly premium will be. Standard renters insurance policies will cover your tenants' belongings, such as:

- Clothes

- Electronics

- Furniture and appliances

- Other basic possessions

The policy will also typically cover high-value property, such as jewelry, for an extra fee.

2. Liability

Your tenants probably don't anticipate an accident to occur at their home, but anything can happen. The liability coverage in their renters insurance policy will cover them and you in case of the following.

- Injury to guests: While renters insurance does not cover injuries to the tenants themselves, it will cover any injuries to their guests or passersby. This coverage allows both landlords and tenants to avoid costly injury-related lawsuits and medical expenses.

- Dog bites: If you allow your tenants to have pets, their renters insurance will cover pet-related injuries and damages, including dog bites. However, some breed restrictions may apply.

- Third-party property damage: If a tenant damages your property, their renters insurance will cover the cost of the repairs or replacement. Imagine they burned the stovetop cooking, or destroyed the wall or a door in the unit when trying to attempt a DIY project. Rather than having to charge the tenant for these potentially expensive damages or eat the cost yourself, their insurance company will foot the bill.

3. Temporary Living Expenses

If a fire or other disastrous event leaves your property inhabitable for a certain period, your tenants' renters insurance will cover their temporary living expenses. They will typically assist in finding a place for your tenants to stay, as well. This coverage lifts the burden of providing tenants with temporary housing off landlords' and property managers' shoulders.

4. Add-Ons and Other Extra Coverage

While renters insurance policies will cover almost all of your tenants' personal belongings and liability, there are a few exceptions. Your tenants may want to consider adding the following types of extra coverage if they apply.

- Storage units: If you or your tenants have a storage unit on the property or in a separate location, some renter insurance companies may allow you to add coverage for the belongings inside for an additional fee.

- Certain breeds of dogs: Some insurance companies may refuse to cover injuries and damages from certain breeds of dogs, or may require renters to pay an additional fee. Be sure to tell any tenants with dogs to verify their policy will cover their pets.

- Jewelry and other valuables: If any of your tenants' belongings are of significant value, they can often add individual coverage just for those possessions, including belongings such as jewelry, musical instruments, collections and other high-value items. Having additional coverage for valuable belongings allows them to use their standard personal property coverage to replace things like their clothes and furniture in a fire or other situation that leads to large-scale loss.

What Doesn't Renters Insurance Cover?

Be sure your tenants are clear on what their renters insurance policies will and will not cover. For example, a few common situations and items renters insurance will not cover include:

- Floods

- Pest infestation such as bedbugs

- Electronics or other belongings that get broken due to wear or misuse

Should I Require Renters Insurance?

Some landlords may be wary about requiring renters insurance for their properties due to the assumption that it will scare away potential tenants. While this may be true, you may also want to ask yourself — do you want a tenant who can't afford another small monthly payment to ensure the safety of their belongings?

The only reason not to require renters insurance is if the laws in your state prohibit you from doing so. In the United States, this is only the case in Oklahoma, where landlords cannot require their tenants to purchase a policy. However, this does not mean you cannot strongly encourage them to do so, and answer the question, "Is renters insurance worth it?" in their rental agreement.

Even if you don't live in Oklahoma, though, be sure to research the laws on renters insurance in your state. While all other states do allow landlords to require renters insurance of some form, there may be additional stipulations or specifications to follow.

How Much Is Renters Insurance?

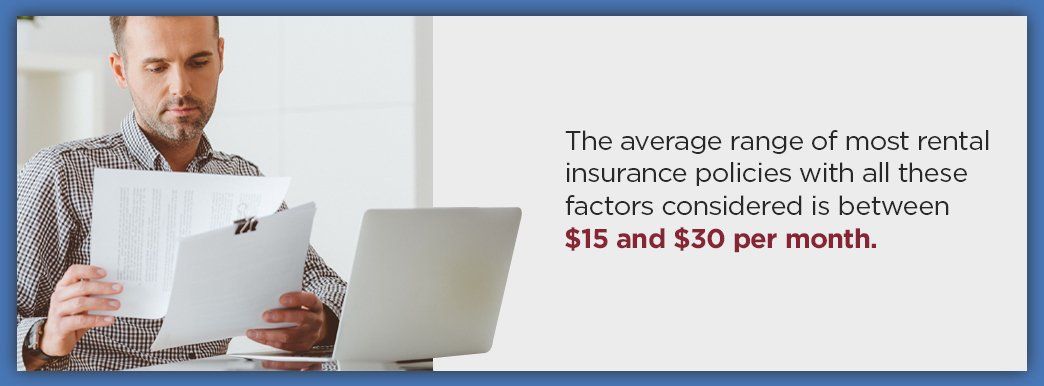

As with any insurance policy, the costs will vary based on the types and amount of coverages your tenants choose, as well as their deductibles and credit history. Rates will also vary depending on the location of your property, the type of property and whether or not your tenants have pets. However, the average range of most rental insurance policies with all these factors considered is between $15 and $30 per month.

Annually, the average cost of renters insurance in the U.S. is $187, depending on which state you live in. For example, an average tenant in South Dakota pays around $118 a year, compared to the $244 price tag Mississippi residents would pay for the same coverage.

Depending on where your tenants choose to purchase their renters insurance policy, they may be able to get a lower monthly rate by bundling their plan with their auto insurance policy. They could also have the option to save by paying for a full year of coverage up front, rather than month to month. Encourage your tenants to do their research and choose the company that gives them the best coverage for their needs at the most affordable price.

How Much Coverage Should My Tenants Purchase?

The amount of coverage your tenants should purchase will depend on a few factors, such as the value of their belongings, the type of dwelling and how much they're willing to pay per month for their insurance policy. The higher the amount of coverage, the higher their premiums will be. Similarly, the lower their deductibles are, the higher their premiums will be.

In general, your tenants will be able to choose their coverage amounts for the following.

- Personal property coverage: The average person renting a two-bedroom apartment has about $20,000 worth of belongings landlords' insurance policies do not cover, and many people's valuables add up to an even higher number. For this reason, the minimum amount of personal property coverage most leases require is around $20,000 or $30,000. Tenants with more valuable possessions may want to consider bumping up their coverage to be safe, as long as they can afford a higher premium. Encourage your tenants to create an inventory of their belongings to decide how much personal property coverage to purchase.

- Personal liability coverage: Typical renters insurance policies will usually include around $100,000 of personal liability coverage, which will be enough to cover most standard claims or incidents. However, if something more serious were to happen in a tenant's unit, such as a severe or life-threatening injury to a guest, medical costs and potential lawsuit expenses could quickly surpass that figure. Most of the time, tenants can increase their liability coverage to between $300,000 and $500,000 for only a few dollars more each month, which may be worth the additional peace of mind. It all depends on your tenants' budget, needs and risk tolerance.

Like with any other insurance policy, your tenants will also be able to choose their deductibles for each coverage type, which is the money they must pay out of pocket when they make a claim. This rate will, in turn, affect their premiums. For example, a plan with a $500 deductible for personal property claims will have a higher monthly premium than a plan with the same amount of coverage but a $1,000 deductible. So, if your tenants would prefer to save money on their premium now, rather than later, when they must make a claim, they should pick a plan with a higher deductible — and vice versa.

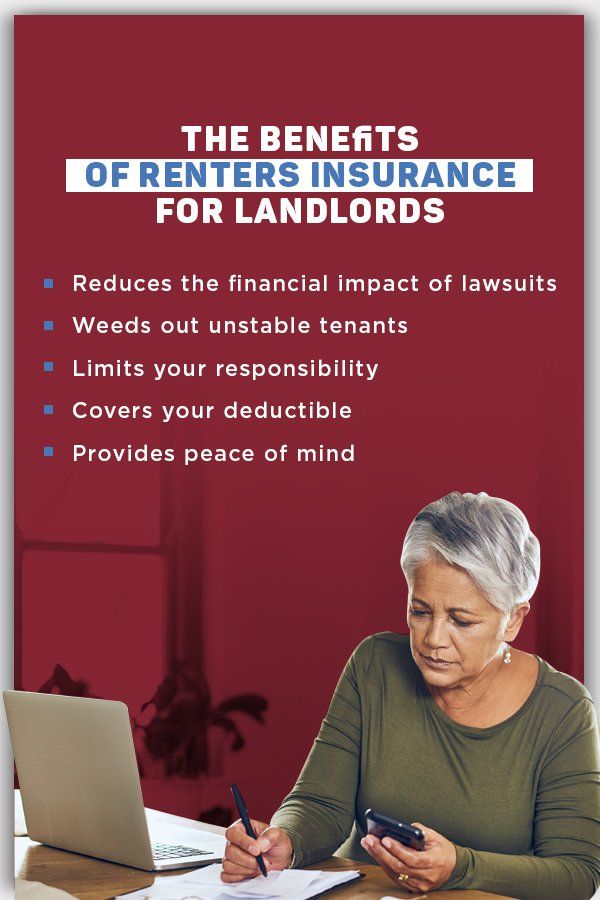

The Benefits of Renters Insurance for Landlords

Several benefits of renters insurance exist for tenants — such as having protection for your belongings and liability coverage in case of any damages or injuries that occur in your home — landlords will also enjoy many advantages to requiring renters insurance for their properties. Some of these benefits include the following.

- Reduces the financial impact of lawsuits: Perhaps the most convincing reason to require your tenants to purchase renters insurance is because of the additional layer of legal protection it offers both you and them. The financial ramifications of any lawsuit can be devastating for both your tenants and you as the landlord. The liability aspect of renters insurance will cover the cost of any bodily injuries your tenants' guests may receive on your property, as well as dog bites for most policies. Renters insurance will also cover the cost of legal representation and any damages awarded — up to your policy limit.

- Weeds out unstable tenants: As long as your tenants are financially stable, they should have no issue spending a few extra bucks each month on protecting themselves and their belongings. If the lease's stipulation requiring tenants to purchase renters insurance scares away potential occupants, you probably wouldn't want them to rent the property anyway. These people are more than likely living from paycheck to paycheck, so what are the odds they'll be able to pay their rent on time each month?

- Limits your responsibility: If a fire or another peril occurs at your property, you may feel responsible for assisting your tenants in finding a temporary living situation, and you may even feel as if you should help replace some of their lost possessions. When you require them to have renters insurance, you can pass off this responsibility to the insurance company. The company will handle finding and funding a temporary living arrangement for your tenants, so you can focus on rebuilding after the incident.

- Covers your deductible: Even if your insurance company covers the cost of some of the damages caused in a fire, burglary or other peril, you will still be responsible for paying the deductible — unless, however, your tenants have renters insurance. Deductibles for homeowner insurance policies can be significant chunks of change, so having a renters insurance policy to cover that makes the unfortunate situation just a little bit easier to handle.

- Provides peace of mind: With all these benefits, another advantage of renters insurance comes to the forefront — the added peace of mind you get knowing you and your tenants have protection! You won't have to deal with tenants thinking you're responsible for replacing their damaged or stolen belongings, and you'll be able to remain financially stable in the event of perils or lawsuits.

Add a Renters Insurance Requirement to Your Leases With Help From Harrisburg Property Management Group

Landlords in Pennsylvania can legally require their tenants to purchase some form of renters insurance. Rather than leaving your tenants wondering, "Do I need renters insurance?" consider requiring them to do so — and be prepared to explain that it's for their benefit, as well as yours.

Do you need a reliable property management company in Harrisburg, PA? Harrisburg Property Management Group is the partner you have been looking for. Our team and our legal counsel can assist you with adding a renters insurance requirement to your lease. Read more about our property management services, or contact us today to speak with a team member.